Get 7% On Your Cash

“Economists say there’s no such thing as a free lunch, but I-bonds offer a guarantee from the U.S. government that you can recover your original capital plus any increases in the official cost of living along the way,” Jason Zweig

“Milton Friedman used to argue that there is no such thing as a free lunch, but at some level this has to be false. The universe exists – who had to pay for it?” Tyler Cowen

One of the cornerstones of personal finance is that you should have an emergency fund. Approximately 3 to 6 months of expenses saved and invested in a safe way that can be drawn upon when you need it. While this amount differs depending on an individual’s personal situation, for most readers, $50,000 or $60,000 should do it.

One drawback of an emergency fund is that banks pay you nearly zero on your cash while at the same time inflation is everywhere. If your emergency fund is not invested in a way to keep pace than the government is actively decreasing the value of your emergency fund every year. This is why Ray Dalio quipped that “cash is trash.”

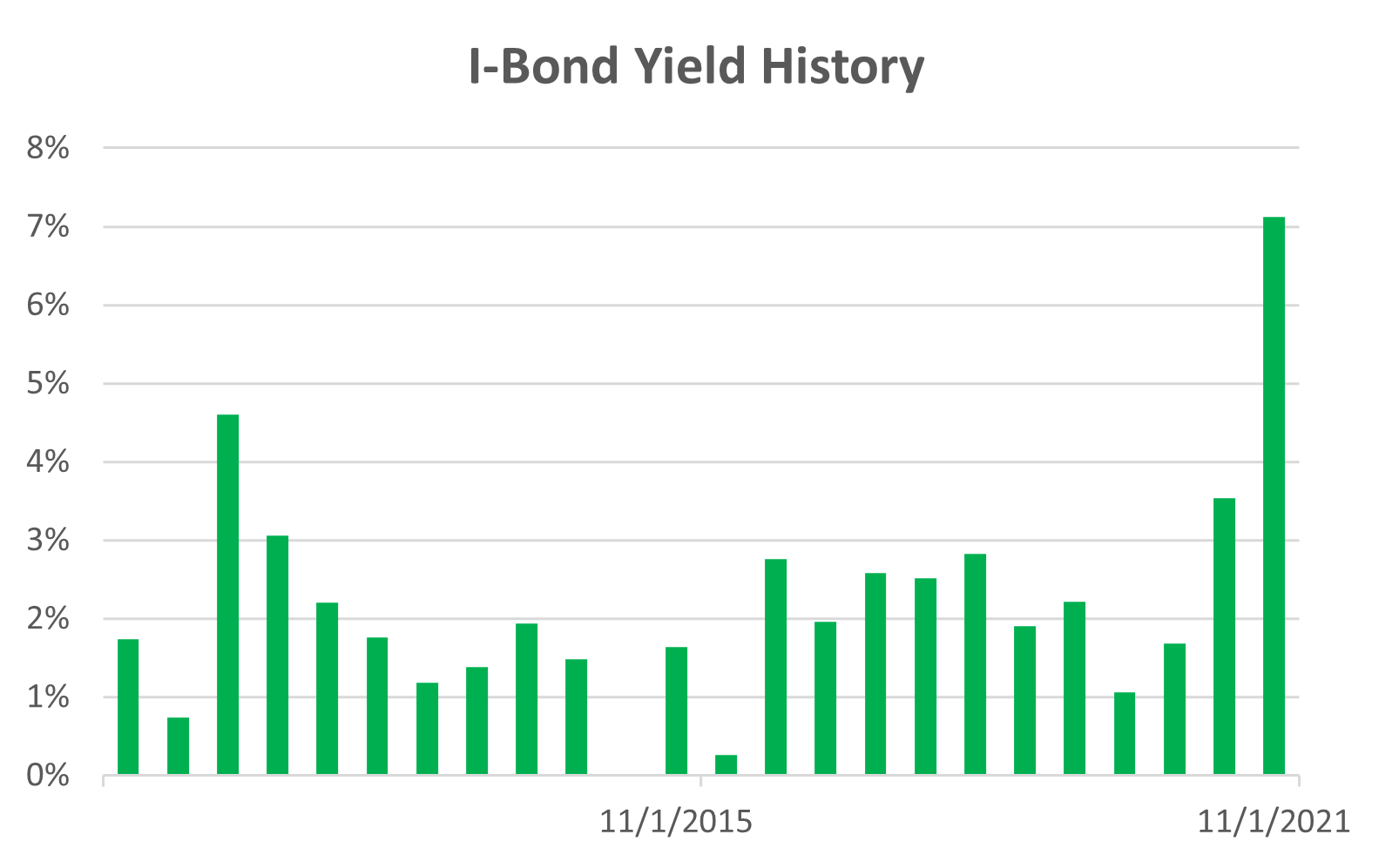

Mr. Dalio may be right, but then inflation bonds are gold. Inflation bonds are the perfect, not widely known, solution to the zero interest rate problem. I-bonds are offered directly from the US government at Treasury Direct and currently pay 7%.

The only downside of I-bonds are that the maximum you are allowed to buy in a given year is $10,000 per person. If this amount was unlimited it would dramatically change markets for the better. Effectively, if you could buy bonds guaranteeing you a fixed rate plus the inflation rate it would eliminate the government’s incentive and preference to inflate away a large debt stock. Count me in if there is ever a proposal to eliminate the cap. In the mean time, there is at least a bit of a work around: you are allowed to buy $10,000 per year per person. So a family of four can buy $40,000 per year, just about equal to a full emergency fund. We will lay out the key details of inflation bonds below:

- Risk: As close to zero as it gets. The bonds are always redeemable at par, meaning the principal is never at risk. Treasury Inflation Protected Securities or TIPS can offer negative yields if inflation goes negative (deflation). I-bonds yield can never go below zero.

- Return: The return from now until April, 2022 is 7.12%. The rate gets reset every 6 months. If inflation remains the same your rate won’t change. If inflation rises you will get paid more. If inflation falls your return will be less, but that also means your money elsewhere lost less of its value. The rate was previously 3.54% before it rose to 7.12%. I’m guessing that both rates are much better than what your savings are earning at the bank (0%).

- Taxes: inflation bonds are state and local tax free. This is a big deal in California with a top state income tax rate of over 10%. It’s an even bigger deal for New Yorkers who face double digit state tax rates and city taxes. If you elect to take your tax refund, if you get one, in the form of an I-bond you can purchase >$10,000 in a calendar year to the tune of the refund. You can choose to defer declaring your interest, and thus paying fedral tax, until you redeem or mature.

- Time: You are required to leave your money in an I-bond for one year. If you withdraw your money after one year, but before 5 years, your penalty is 3 months of interest. This would turn your 7.12% return into 5.34%. Still great.

- Minor Accounts: the annual gift tax exclusion is currently $15,000 per recipient per year, rising to $16,000 in 2022. The $10,000 annual maximum I-bond purchase per individual per year fits nicely under this threshold. Withdrawals of minor accounts are allowed as long as they benefit the minors. You link your kids’ accounts to yours through Treasury Direct.

Source: US Treasury, yield shown 6-monhs after issuance

My family’s emergency fund is going into I-bonds. I like the idea that Uncle Sam will be buying each of my family members a plane ticket to Greece next Summer, rather than having to pay for it myself.